Veterinary Software Market Size, Share & Industry Analysis, By Type (Practice Management Software, Clinical Workflow Software, Diagnostic Imaging Software, Client Engagement Software, Scheduling/Online Booking Software, Telemedicine / Virtual Care Software, Revenue Cycle Software, AI Documentation/Dictation/Scribe Software, and Others), By Deployment (Cloud-based, On-Premise/Server-based, and Hybrid), By Animal Type (Companion and Livestock), By End User (Veterinary Hospitals & Specialty/Referral Centers, Independent Veterinary Practices, and Others), and Regional Forecast, 2026-2034

Veterinary Software Market Size and Future Outlook

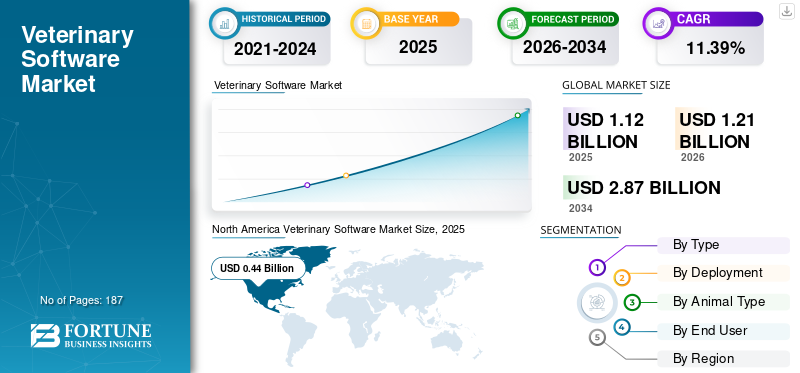

The veterinary software market size was valued at USD 1.12 billion in 2025. The market is projected to grow from USD 1.21 billion in 2026 to USD 2.87 billion by 2034, exhibiting a CAGR of 11.39% during the forecast period.

The market encompasses various software systems utilized by the veterinary clinics, specialty/referral facilities, and independent practices to oversee daily operations and enhance care delivery. The market is influenced by increasing demand for cloud-based veterinary systems, a heightened necessity to lessen front-desk and documentation burdens, wider utilization of integrated booking and communication tools, and a more robust adoption of workflow and payment software in companion-animal practices. The market expansion is additionally driven by the transition from simple standalone systems to interconnected software environments that unify records, client interactions, workflows, and payments in a single platform.

Key players in the market include IDEXX Laboratories, Covetrus, Vetstoria, Otto, Provet Cloud, Shepherd Veterinary Software, and others. These firms are concentrating on integrated cloud deployment, connected client-facing workflows, and AI-enabled documentation that helps clinics save time, improve throughput, and scale recurring software usage.

Download Free sample to learn more about this report.

VETERINARY SOFTWARE MARKET TRENDS

Growing Use of AI in Diagnostics and Imaging is a Significant Trend Observed in Market

The increasing application of AI in veterinary diagnostics and imaging is becoming a significant trend in the market. Veterinary clinics are progressively integrating AI-powered imaging technologies to accelerate diagnosis, improve image clarity, and facilitate quicker clinical decision-making, particularly in radiology-intensive procedures. This trend is becoming more robust as clinics face pressure to manage increasing caseloads with a restricted workforce, increasing the value of automation and decision-support tools. AI enhances workflow efficiency by combining image capture, interpretation assistance, and interconnected software platforms into a single digital process. Consequently, AI-driven imaging is transitioning from a specialized function to a wider commercial feature within sophisticated veterinary software solutions.

This is particularly critical for hospitals and specialty/referral centers, where the complexity of diagnostics and volume demand is higher. The trend additionally fosters increased software expenditure for each site, as AI-driven imaging is generally integrated with core practice management and workflow systems. The increasing implementation of AI in diagnostics and imaging is assisting veterinary practitioners in enhancing care standards while simultaneously boosting the strategic importance of software in everyday tasks. These factors are supporting the overall veterinary software market growth.

- For instance, in January 2026, DEXX Laboratories launched the ImageVue DR50 Plus Digital Imaging System which combines a connected imaging ecosystem with AI-powered imaging to help accelerate diagnosis and improve care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Adoption of Cloud-Based Veterinary Software is Propelling Market Growth

The growing usage of cloud based solutions is a major factor propelling the market growth. Cloud platforms are becoming more popular as they lessen reliance on local servers, decrease IT upkeep requirements, and simplify access for clinics to records, scheduling, billing, and workflow tools from various locations. This is vital for practices with multiple doctors, specialty centers, and expanding veterinary groups requiring adaptable systems and simplified software upgrades. Cloud deployment enhances integration among functions including client communication, payments, workflow, and reporting, thus boosting the overall software value per site. Moreover, cloud models facilitate ongoing subscription income for vendors and simplify the process for clinics to integrate additional modules gradually. With veterinary practices placing greater emphasis on operational efficiency, remote access, and integrated workflows, cloud-based solutions are increasingly favoring the deployment approach. All these factors cumulatively drive the overall market growth.

- For instance, in January 2025, Covetrus announced that is has advanced the Covetrus Platform as a comprehensive and connected offering designed for modern veterinary practices, centered on cloud-based practice technology and integrated operational tools.

MARKET RESTRAINT

High Switching Costs and Legacy-System Dependence to Restrict Market Expansion

Significant switching costs and reliance on legacy systems serve as a distinct limitation on the market. Numerous clinics continue to use traditional server-based systems, as the transition to modern cloud platforms frequently necessitate data migration, staff retraining, workflow redesign, hardware assessments, and temporary disruptions in operations. Concurrently, vendors advocating for cloud migration recognize that software changes necessitate preparation concerning team preparedness, IT readiness, and logistics, potentially hindering decision-making and prolonging sales cycles. This creates a larger obstacle for busy practices that cannot sustain downtime or loss of productivity during the implementation process. Consequently, numerous clinics postpone replacement choices and persist in prolonging the lifespan of outdated platforms rather than upgrading right away. This hinders the rate of cloud migration and decreases the speed at which vendors can transition the market to more advanced, valuable software ecosystems.

- For instance, zyVet’s software transition guidance, actively published on its current site in 2026, which states that practices need to prepare their teams, IT systems, and logistics for a successful software transition, and notes that ezyVet helps only 2–3 veterinary businesses move to the cloud every week.

MARKET OPPORTUNITIES

Rising Demand for Telemedicine and Remote Consultations to Offer New Growth Opportunities

Increasing demand for telehealth and virtual consultations is generating a significant market opportunity. Veterinary clinics are progressively seeking virtual-care solutions to enhance accessibility, manage follow-up cases more effectively, and minimize unnecessary visits to the office. This holds significant value for active companion-animal clinics, distant pet caregivers, follow-ups after treatment, behavior assessments, and triage assistance. Telemedicine aids clinics in utilizing staff time more effectively by transferring appropriate interactions to digital platforms, ensuring that in-person resources are concentrated on more critical cases. As client demands shift toward convenience and quicker communication, vendors have increased opportunities to enhance integrated telemedicine, scheduling, messaging, and documentation functions within larger veterinary software systems. The opportunity is expanding as remote consultations can enhance client retention and foster continuity of care when utilized within suitable regulatory and clinical limits. All these factors would drive the market growth during the forecast period.

- For instance, in November 2025, the AVMA Board updated the telemedicine policies which shows that organized veterinary medicine is still actively refining the framework for telemedicine use in practice.

MARKET CHALLENGES

Cybersecurity and Data-Protection Risk Pose a Prominent Challenge to Market Growth

The risk of cybersecurity and data protection poses a significant challenge for the market. As practices convert patient records, imaging, payments, communication, and cloud processes to digital formats, they face increased risks of cyberattacks, ransomware, and patient data loss incidents. This imposes an additional strain on software vendors and clinics as they are required to allocate resources for enhanced security measures, employee training, backup solutions, and incident-response strategies in addition to standard software expenses. For smaller and independent practices, these additional expenses may postpone the embrace of advanced connected platforms or hinder the transition to newer cloud systems. Moreover, cybersecurity risks lead to increased caution among buyers when assessing vendors, particularly when software manages client data, payment details, and medical records. These factors cumulatively affect the market growth.

- For instance, in April 2024, CVS Group published a Notice of Cyber Incident related to unauthorized external access to a limited number of its IT systems caused “considerable operational disruption” and led it to take parts of its IT systems offline.

Segmentation Analysis

By Type

Broad Utility Across Wide Range of Daily Functions Supported Practice Management Software Segmental Dominance

In terms of type, the market is divided into practice management software, clinical workflow software, diagnostic imaging software, client engagement software, scheduling/online booking software, telemedicine/virtual care software, revenue cycle software, AI documentation/dictation/scribe software, and others.

The practice management software segment dominated the global market in 2025. This can be attributed to broad usage of these software for various daily operations, covering appointment scheduling, patient records, billing, inventory, treatment history, and reporting across end users. Its supremacy is further reinforced by the reality that numerous related tools including client communication, payments, workflow, and documentation typically link back to the practice management platform instead of substituting it. Additionally, practices typically prioritize investing in practice management software initially before integrating add-on modules, establishing it as the essential purchase within the software stack. Moreover, strategic initiatives undertaken by operating players also supports the segment dominance.

- For instance, in January 2026, Instinct Science announced acquisition of ScribbleVet, stating that the combination would redefine veterinary practice management software by embedding AI, workflow, and clinical intelligence into a single system.

The AI documentation/dictation/scribe software segment is anticipated to rise with a CAGR of 26.50% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Uptake of Cloud-based Solutions Led to Segment Dominance

Based on deployment, the market is classified into on-premise/server-based, hybrid, and cloud-based.

The cloud-based segment led the global market in 2025. The veterinary clinics are progressively opting for software that is more accessible, updatable, and scalable across various locations without relying on local servers and extensive IT assistance. The prominence of this segment is bolstered by the increasing demand for immediate access to patient records, schedules, billing, and workflow tools from any location, particularly in practices with multiple doctors and expanding veterinary organizations. Moreover, cloud-based systems are increasingly favored due to their ability to simplify software updates, data backups, integrations, and remote access compared to conventional server-based systems. Also, new product launches by key players is anticipated to strengthen the segment’s share in the market. The segment is set to hold 58.0% share in 2026.

- For instance, in December 2025, Instinct Science launched Instinct EMR for Primary Care, describing it as a next-generation cloud-based practice management system designed for busy general practices.

The hybrid segment is anticipated to rise with a CAGR of 12.72% over the forecast period.

By Animal Type

Large Base of Companion Animals Supported Segmental Dominance

On the basis of animal type, the market is divided into companion and livestock.

The companion segment captured the largest veterinary software market share in 2025. This is due to most veterinary software spending is concentrated on pet-care settings where clinics need practice management, appointment scheduling, client communication, billing, workflow, imaging, and documentation tools on a daily basis. Additionally, its dominance is supported by the large and growing base of companion-animal visits, stronger spending per clinic, and wider use of multi-module software platforms in small-animal practices compared with livestock settings. In addition, companion-animal clinics usually adopt a broader digital stack as they manage higher volumes of appointments, follow-ups, preventive care, and owner communication. Furthermore, the segment is set to hold 86.1% of share in 2026.

- For instance, in January 2026, Mars Veterinary Health published its 2025 Science Impact Report, highlighting advances in pet health across its globally connected veterinary care network.

The livestock segment is anticipated to rise with a CAGR of 10.52% over the forecast period.

By End User

Broad Customer Base of Independent Veterinary Practices Supported Segment Growth

Based on end user, the market is segmented into veterinary hospitals & specialty/referral centers, independent veterinary practices, and others.

The independent veterinary practices segment dominated the market in 2025. These practices represent the broadest customer base and account for a large share of routine veterinary software purchases across scheduling, patient records, billing, client communication, and day-to-day workflow management. Its dominance is being supported by the fact that most veterinary clinics operate as independent practices and usually adopt software first to improve front-desk efficiency, manage appointments, reduce administrative burden, and support better client service. In addition, independent clinics rely heavily on core practice management systems as they need one platform to handle both clinical and business operations with limited staff. The segment is also benefiting from growing demand for affordable cloud-based tools that help smaller practices improve productivity without building large internal IT capabilities. Furthermore, the segment is set to hold 57.2% share in 2026.

- For instance, in September 2025, Covetrus announced that its VetSuite network for independent veterinary practices had delivered more than USD 30 million in realized savings since launch and was already serving 1 in 10 companion animal veterinarians nationwide.

In addition, veterinary hospitals & specialty/referral centers are projected to withness 13.02% growth rate during the forecast period.

Veterinary Software Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, Latin America, North America, and the Middle East & Africa.

North America

North America Veterinary Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached a value of USD 0.41 billion in 2024 and dominated the global market. In 2025, the region maintained its leading position, with USD 0.44 billion revenue share. Largest installed base of veterinary practices, high pet-care spending, and the strongest adoption of cloud-based and multi-module software are some of the prominent factors driving the regional market growth.

U.S. Veterinary Software Market

The U.S. market led the North American region and is projected to be approximately USD 0.41 billion in 2026, representing about 34.1% of the global market.

Europe

Europe market is anticipated to grow at 9.75% CAGR during the forecast period. European region is growing due to its large veterinary workforce, increasing clinic scale, and rising need for digital efficiency tools. Additionally, the growth is also supported by a gradual shift toward cloud-based platforms and stronger software use in multi-vet and corporate practice settings.

U.K. Veterinary Software Market

The U.K. market in 2026 is estimated at around USD 0.06 billion, representing roughly 4.9% of global revenues.

Germany Veterinary Software Market

Germany market is projected to reach approximately USD 0.06 billion in 2026, equivalent to around 4.6% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.32 billion by 2026. Rising companion-animal care, growing clinic digitization, and increasing adoption of cloud-based veterinary systems in both developed and emerging markets are key growth drivers in this region.

Japan Veterinary Software Market

The Japan market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 4.9% of global revenues.

China Veterinary Software Market

China’s market is projected to reach revenues of around USD 0.08 billion in 2026, representing roughly 6.9% of global sales.

India Veterinary Software Market

The India market in 2026 is estimated at around USD 0.03 billion, accounting for roughly 2.7% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are predicted to witness a slower growth over the study period. The Latin America market is growing due to large and expanding veterinary ecosystem, especially in Brazil, along with gradual modernization of clinic operations. The Latin America market in 2026 is estimated at around USD 0.05 billion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.02 billion by 2026, representing about 1.3% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Product Integration and Expanding AI-Enabled Workflow Capabilities Strengthens Market Position of Key Companies

The market features a moderately fragmented competitive landscape led by established platform vendors and fast-growing emerging companies. Prominent players in the market include IDEXX Laboratories, Inc., Otto, Covetrus, Patterson Veterinary (NaVetor), and Shepherd Veterinary Solutions. These companies are focusing on AI-powered workflow enhancement, deeper PIMS integration, and more unified software stacks that improve both operational efficiency and client experience.

- For instance, in January 2025, Covetrus announced AI-powered workflow automation and treatment board capabilities within Covetrus Pulse as part of advanced Covetrus Platform.

Other significant participants include Vetstoria, Carestream Health, Nordhealth, Animal Intelligence Software, and others. These firms are anticipated to focus on innovating new products, forming collaborations and partnerships, and developing scalable data platforms to enhance their competitive standing throughout the forecast period.

LIST OF KEY VETERINARY SOFTWARE COMPANIES PROFILED

- IDEXX Laboratories, Inc. (U.S.)

- Otto (U.S.)

- Covetrus (U.S.)

- Patterson Veterinary (NaVetor) (U.S.)

- Shepherd Veterinary Solutions (U.S.)

- Vetstoria (U.K.)

- Carestream Health (U.S.)

- Nordhealth (Finland)

- Animal Intelligence Software (U.S.)

- Farmbrite (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Otto launched OttoPilot AI-powered business insights and recommendations for veterinary clinics, expanding its AI workflow and analytics capabilities.

- January 2026: Digitail introduced Tails AI Vision, enabling its AI assistant to analyze, summarize, and extract data from images and PDF files for veterinary practices.

- January 2026: Digitail raised USD 23 million Series B funding for the acceleration of expansion in veterinary practice management software and further advance AI capabilities for veterinarians and pet parents.

- November 2025: Vetstoria announced integration with Reserve with Google, extending veterinary online booking visibility and access through Google.

- February 2024: IDEXX Laboratories Inc. launched Vello, a pet owner engagement software solution designed to connect veterinary practices and clients through digital communication tools.

REPORT COVERAGE

The global veterinary software market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, technological advancements, as well as key developments in the industry within the market. The market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.39% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Deployment, Animal Type, End User, and Region |

| By Type |

|

| By Deployment |

|

| By Animal Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.12 billion in 2025 and is projected to reach USD 2.87 billion by 2034.

In 2025, the North America market value stood at USD 0.44 billion.

The market is expected to exhibit a CAGR of 11.39% during the forecast period of 2026-2034.

By type, the practice management software segment is expected to lead the market.

Increasing adoption of cloud-based veterinary software coupled with shift toward integration with EHR systems are primarily driving market expansion.

IDEXX Laboratories, Inc., Covetrus, Patterson Veterinary (NaVetor), and Shepherd Veterinary Solutions are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us