Missile Interceptors Market Size, Share & Industry Analysis, By Threat Type Intercepted (Ballistic Missile Threats, Cruise Missile Threats, Hypersonic Threats, and Complex Raid Threats), By Defense Interceptor Type (Point, Lower-Tier Terminal Ballistic Missile, Multi-Mission Air-and-Missile, High-Altitude BMD, Strategic Homeland, Anti-Hypersonic, and Ascent-Phase Interceptors), By Platform (Land-Based Mobile, Sea-Based, Space-Based), By Interceptors Technology, By Range (Short Range, Medium Range, Long Range, Extended-Range, & Strategic Homeland Defense) and Regional Forecast, 2026-2034

Missile Interceptors Market Size and Future Outlook

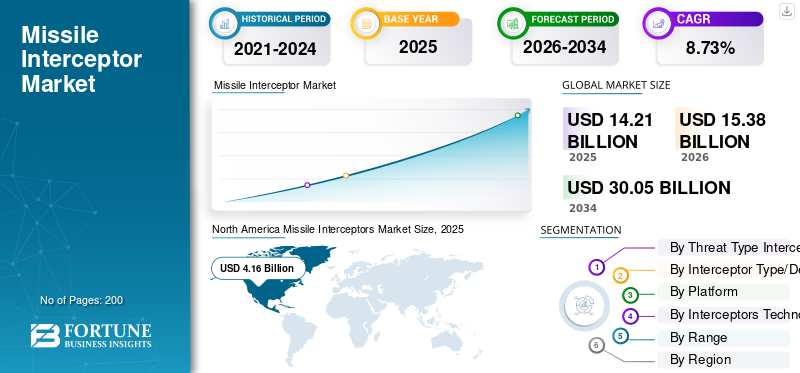

The missile interceptors market size was valued at USD 14.21 billion in 2025. The market is projected to grow from USD 15.38 billion in 2026 to USD 30.05 billion by 2034, exhibiting a CAGR of 8.73% during the forecast period. North America dominated the missile interceptors market with a market share of 29.28% in 2025.

The market encompasses systems designed to detect, track, and destroy incoming threats such as ballistic, cruise, and hypersonic missiles, typically using kinetic kill or blast fragmentation warheads guided by radar and electro optical sensors combined with solid‑propellant propulsion. These interceptors are deployed in multi layered air and missile defense architectures for point and area defense of cities, military bases, and naval platforms, driven by rising geopolitical tensions, proliferation of advanced missiles, and higher national defense outlays.

Key players in the market include Lockheed Martin (Patriot, THAAD and SM‑3 interceptors), Raytheon (SM‑3, SM‑6, ESSM), Northrop Grumman (Ground‑Based Interceptor, NGI), Rafael (Iron Dome Tamir, David’s Sling Stunner, Arrow‑3), and BAE Systems (subsystems and electronics for systems such as Aster), all investing in advanced sensors, guidance, and multi‑mission interceptors.

Download Free sample to learn more about this report.

MISSILE INTERCEPTORS MARKET TRENDS

Integration of Network Integrated Sensors is Emerging Market Trend

There is a shift toward indoor and GPS denied navigation using vision based positioning, driven by the need to operate drones, robots, and autonomous vehicles where satellite signals are weak or absent. Visual Simultaneous Localization and Mapping (SLAM) and vision based localization systems increasingly fuse cameras, IMUs, and sometimes LiDAR or Ultra-Wideband (UWB) to deliver stable, real time positioning in warehouses, tunnels, urban canyons, and indoor facilities. These optical centric stacks are favored as they require fixed infrastructure, can map unfamiliar environments on the fly, and support emerging applications such as autonomous inspection, logistics, and mixed‑reality navigation beyond traditional GNSS dependent schemes.

Download Free sample to learn more about this report.

Impact of Russia Ukraine War

The Russia Ukraine war has highlighted the need for greater stockpile resilience, improved sensor‑fusion and battle‑management integration, and a diversified mix of interceptors alongside non‑kinetic interception capabilities. It has also accelerated battlefield driven innovation in lower cost, drone based intercept solutions and is reshaping long term defense planning toward more resilient, flexible, and multi‑domain air‑and‑missile‑defense postures.

Impact of Middle East War

The market for missile interceptors has drastically impacted as a result of the ongoing crisis in the Middle East, transitioning from a state of steady procurement to one of high intensity demand and supply chain strain. The conflict has also driven greater investment in multi‑layered air‑defense concepts, including non-kinetic and electronic warfare measures, while reinforcing the importance of forward based radars and globally distributed interceptor deployments to manage regional and beyond regional threats.

MARKET DYNAMICS

MARKET DRIVERS

Rising Geopolitical Tensions is Anticipated to Drive Market Growth

Rising geopolitical tensions are anticipated to drive missile interceptors market growth as states face heightened regional conflicts, cross‑border strikes, and proliferation of advanced missile arsenals. This environment is pushing governments to prioritize air and missile defense, increase defense budgets, and procure larger inventories of interceptors and layered defense systems. Persistent high‑intensity operations in theaters such as the Middle East and Eastern Europe are accelerating demand for new interceptors and expanded production capacity.

MARKET RESTRAINTS

Stringent Export Controls Limiting Technology Sharing is a Major Market Restraint

Stringent export controls limit technology sharing and act as a key market restraint in the missile‑interceptor sector by restricting the transfer of sensitive components, software, and production know‑how to allies and partners. Multilateral regimes such as the Missile Technology Control Regime (MTCR) treat many missile technologies as Category I or II items, subjecting transfers to strong presumption‑of‑denial reviews and licensing hurdles. These controls slow down cooperative development programs, constrain local industrialization efforts in emerging defense‑producing states.

MARKET OPPORTUNITIES

Rise in Government Investments Creates New Market Opportunities

Rising government investments are creating a new market opportunity for missile‑interceptor producers as countries increase defense budgets and prioritize multi‑layered air and missile defense modernization. National‑industrial policies in countries such as India that combine growing defense expenditures with “Make in India” programs and incentives are further opening opportunities for domestic and foreign firms to co‑produce interceptors and subsystems.

MARKET CHALLENGES

High Unit Cost is a Key Market Challenge

High unit costs a major market challenge in the missile‑interceptor sector as advanced interceptors can cost several million dollars apiece, vastly exceeding the cost of many attacking missiles or drones. Furthermore, high prices also constrain procurement volumes, limit the number of platforms that can be equipped, and raise questions about long‑term fiscal sustainability for even high defense budgets.

Segmentation Analysis

By Threat Type Intercepted

High Strategic Risk & Proliferation to Boost the Ballistic Missile Threats Segmental Growth

Based on the threat type intercepted, the market is segmented into ballistic missile threats, cruise missile threats, hypersonic threats and complex raid threats.

The ballistic missile threats segment is anticipated to account for the largest missile interceptors market share. The segmental growth is owing to increasing proliferation in number of nations acquiring ballistic missiles due to the high risk ranging from short-range tactical to Intercontinental Ballistic Missiles (ICBMs).

The hypersonic threats segment is anticipated to rise with a high CAGR of 9.17% over the forecast period.

By Interceptor Type/Defense Layer

Adaptability to Diverse Threats Boosts Medium-Tier Area/Multi-Mission Air-and-Missile Defense Interceptors Segment Growth

Based on interceptor type/defense layer, the market is segmented into point defense interceptors, lower-tier terminal ballistic missile defense interceptors, medium-tier area multi-mission air-and-missile defense interceptors, upper-tier terminal/high-altitude BMD interceptors, regional exo-atmospheric/midcourse interceptors, strategic homeland defense interceptors, glide-phase/anti-hypersonic interceptors and boost-phase/ascent-phase interceptors.

In 2025, the medium-tier area/multi-mission air-and-missile defense interceptors segment dominated the global market. These systems are designed to counter ballistic missiles, cruise missiles, and Unmanned Aerial Vehicles (UAVs) simultaneously which makes them ideal for multi-missions.

The glide-phase/anti-hypersonic interceptors segment is projected to grow at a highest CAGR of 9.68% over the forecast period.

By Platform

Cost-Effectiveness of Land-Based Mobile Platforms Propels Segment Growth

Based on the platform, the market is segmented into land-based mobile, sea-based, airborne/boost-phase experimental and space-based/future concept.

The land-based mobile segment is anticipated to witness a dominating market share over the forecast period. The segmental dominate is owing to as Land-based systems are more appealing for large-scale procurement and upgrades as they are frequently more cost-effective than naval or air-based systems.

The Space-Based / Future Concept segment is projected to grow at a high CAGR of 9.87% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Interceptors Technology / Architecture

High Value and R&D Focus to boost the Guidance / Seeker Type Segment

Based on interceptors technology/architecture, the market is segmented into kill mechanism, guidance/seeker type, propulsion/vehicle architecture.

The guidance / seeker type segment dominated the segmental market share. With continuous improvements in radar, sensors, and AI-based target tracking methods, guidance systems are the main factor propelling major growth in interceptors.

In addition, kill mechanism segment is projected to grow at a CAGR of 8.24% during the study period.

By Range

Countering Advanced and Increasing Threats to boost the Extended-Range/Theater Defense Segment

Based on range, the market is segmented into very short range, short range, medium range, long range, extended-range/theater defense and strategic homeland defense.

The extended-range/theater defense segment dominated the segmental market share. Modern adversary is increasingly using sophisticated, longer-range ballistic missiles, cruise missiles, and hypersonic weapons that short-range or point-defense systems cannot engage efficiently.

In addition, strategic homeland defense is projected to grow at a high CAGR of 9.68% during the study period.

Missile Interceptors Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Middle East and Rest of the World.

North America

North America Missile Interceptors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 3.55 billion, and also maintained the leading share in 2025, with USD 4.16 billion. North America, led by the U.S., has the largest market, with major investments in THAAD, Aegis/SM‑3, and Patriot‑based systems, plus the Next Generation Interceptor for homeland defense, fielded by Lockheed Martin, Raytheon, Northrop Grumman, and Boeing under the U.S. Missile Defense Agency.

U.S. Missile Interceptors Market

Based on North America’s strong contribution, the U.S. market can be analytically approximated at around USD 2.72 billion in 2026, accounting for roughly 8.98% CAGR. The U.S. drives the product demand through large‑scale programs such as ground‑based interceptor modernization, Aegis BMD, and THAAD, supported by the missile defense agency and industry leaders.

Europe

Europe is projected to record a steady growth rate during the forecast period of 8.78%, which is the second highest among all regions, and reach a valuation of USD 2.98 billion by 2026. Europe sustains demand via NATO coordinated air and missile‑defense initiatives and national upgrades, particularly in France and Germany, which rely on MBDA’s Aster‑30 and associated systems

U.K. Missile Interceptors Market

The U.K. market in 2026 is estimated at around USD 0.95 billion, representing roughly 9.30% CAGR during the study period. The U.K. participates in European‑wide missile‑defense cooperation and upgrades its point defense and naval systems, with BAE Systems and MBDA integrated platforms.

Germany Missile Interceptors Market

Germany’s market is projected to reach approximately USD 0.80 billion in 2026. Germany is modernizing its air and missile‑defense posture through NATO‑aligned programs and national projects, investing in ground‑based systems integrated with MBDA and Thales‑built components and sensors.

Asia Pacific

Asia Pacific region is estimated to reach USD 3.42 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. Asia Pacific is a fast‑growing missile‑interceptor region, with Japan, South Korea, and Australia deepening cooperation with U.S. Aegis and THAAD deployments, while regional programs focus on layered defenses against regional missile threats, backed by joint R&D and technology‑transfer arrangements with U.S. and European players.

Japan Missile Interceptors Market

The Japan market in 2026 is estimated at around USD 0.62 billion, accounting for roughly 9.23% of CAGR during the forecast period. Japan’s market is growing due to regional missile tests and an evolving threat landscape, which has pushed Tokyo to expand its Aegis‑based fleet and SM‑3 interceptor inventory while accelerating domestic sensor, command‑and‑control, and hypersonic‑related R&D.

China Missile Interceptors Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.10 billion. China is advancing indigenous exo and endo‑atmospheric interceptors through its own BMD program, integrating space‑based early warning and ground‑based sensors to handle regional ballistic and hypersonic threats.

India Missile Interceptors Market

The India market in 2026 is estimated at around USD 0.94 billion. India is expanding its indigenous missile‑interceptor capability via the Ballistic Missile Defense Programme, led by DRDO and supported by firms such as Bharat Dynamics, with phased deployments of PAD/AD‑1 and AD‑2 systems.

Middle East

The Middle East market in 2026 is estimated at around USD 2.43 billion. The Middle East market is expanding rapidly due to persistent cross‑border strikes, drone and missile‑swarm threats, and recent high‑intensity regional wars that have burned large interceptor stocks.

Saudi Arabia Missile Interceptors Market

The Saudi Arabia market in 2026 is estimated at around USD 0.80 billion. Saudi Arabia is strengthening its missile‑interceptor posture through major acquisitions and localization programs, including the introduction of U.S.‑built THAAD batteries and further Patriot‑based deployments to cover key cities and industrial infrastructure.

Rest of the World

The rest of the world market include Africa and Latin America. In the rest of the world, some Latin American and African countries seek limited scale point defense upgrades to protect critical infrastructure and stabilize domestic security environments. The Latin America and Africa market is set to reach a valuation of USD 1.27 billion and USD 0.79 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships Among Key Players fuels Market Competition

The missile‑interceptor market is moderately consolidated, with a small set of large defense primes accounting for the bulk of systems and interceptors deployed globally. Key players include Lockheed Martin, Raytheon, Northrop Grumman, Boeing, Rafael Advanced Defense Systems, MBDA, Thales Group, BAE Systems, Almaz Antey, and Elbit Systems, alongside national entities such as India’s DRDO and China’s state‑owned missile‑defense developers.

Strategic partnerships are a central feature of the competitive landscape, with global primes collaborating with regional defense‑industry partners for co‑production, local assembly, and technology transfer arrangements, especially in Asia, the Middle East, and Europe. Primes also team up with sensor, guidance, and data fusion specialists to integrate advanced EO/IR, radar, and AI‑enabled tracking capabilities into missile‑defense architectures, while joint‑development and interoperability agreements among allies enable shared testing, stocked inventories, and common standard command and control systems.

LIST OF KEY MISSILE INTERCEPTORS COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Raytheon (U.S.)

- Northrop Grumman (U.S.)

- Rafael Advanced Defense Systems (Israel)

- Boeing (U.S.)

- MBDA (France)

- Thales Group (France)

- BAE Systems (U.K.)

- Almaz Antey (Russia)

- Elbit Systems (Israel)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The Department of War announced a framework agreement to triple the production of seekers for the Terminal High Altitude Area Defense (THAAD) interceptor in collaboration with Lockheed Martin and BAE Systems.

- March 2026: Raytheon received a contract worth USD 11.74 billion after additional USD 8.41 billion to supply materials, services, engineering, and product support for Standard Missile-3 Block missile variants for the U.S. and its allies.

- February 2026: L3Harris Technologies has been awarded a new contract worth nearly USD 400 million to manufacture more solid rocket boost motors and Liquid Divert and Attitude Control Systems (LDACS) as a supplier to the contract for the Missile Defense Agency’s Terminal High Altitude Area Defense (THAAD) system.

- November 2024: Mitsubishi Heavy Industries has been awarded a USD 368 million contract by Japan's Ministry of Defense to build the Glide Phase Interceptor (GPI), a next-generation missile defense systems intended to shoot down hypersonic missiles.

- April 2024: A USD 17 billion contract to create the next generation of interceptors to protect the U.S. from an intercontinental ballistic missile assault has been awarded to Lockheed Martin.

REPORT COVERAGE

The missile interceptors market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The market report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.73% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Threat Type Intercepted, Interceptor Type/Defense Layer, Platform, Interceptors Technology/Architecture, Range, and Region |

| By Threat Type Intercepted |

|

| By Interceptor Type/Defense Layer |

|

| By Platform |

|

| By Interceptors Technology/Architecture |

|

| By Range |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 14.21 billion in 2025 and is projected to reach USD 30.05 billion by 2034.

In 2025, the North America market value stood at USD 4.16 billion.

The market is expected to exhibit a CAGR of 8.73% during the forecast period of 2026-2034.

By platform, the guidance/seeker type segment is expected to dominate the market.

Rising geopolitical tensions is anticipated to drive market growth.

Lockheed Martin, Raytheon, Northrop Grumman, Rafael Advanced Defense Systems, Boeing are few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us