Medical Electronics Market Size, Share & Industry Analysis By Product Type (Diagnostic Imaging Devices [MRI, X-ray, CT, IVD Analyzers, and Others], Patient Monitoring Devices [Blood Glucose Monitors, Cardiac Monitors, Hemodynamic Monitors, and Others), and Therapeutic Devices [Surgical & Operating Room Electronics, Life Support Devices, and Others]), By Component (Sensors, Microprocessors/Microcontrollers, Memory Devices, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Diagnostic Laboratories, and Others), and Regional Forecast, 2026-2034

Medical Electronics Market Overview

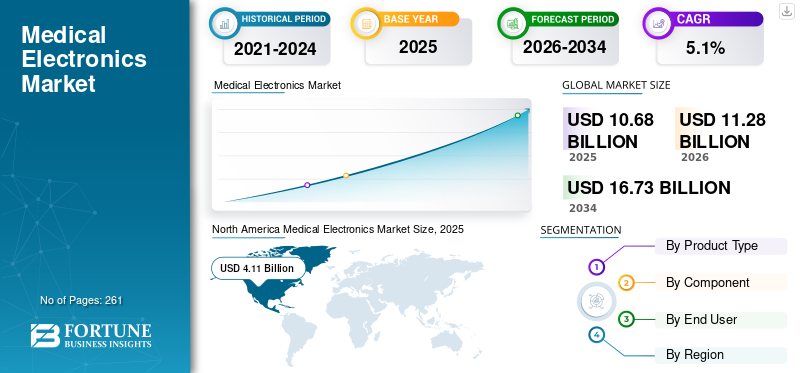

The global medical electronics market size was valued at USD 10.68 billion in 2025. The market is projected to grow from USD 11.28 billion in 2026 to USD 16.73 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. North America dominated the medical electronics market with a market share of 38.48% in 2025.

Medical electronics are electronic instruments and devices used for the diagnosis and treatment of diseases among the patient population. The rising incidence of chronic illnesses, growing need for advanced diagnostic solutions, and ongoing development of healthcare infrastructure are driving higher adoption of these devices across the market. Additionally, the expanding elderly population is accelerating the use of diagnostic and therapeutic solutions, further strengthening overall product uptake.

- As per the 2024 data published by the Centers for Disease Control & Prevention (CDC), in the U.S. about 1 in 20 adults aged 20 and older have coronary artery disease.

Moreover, increased integration of advanced technologies by key industry players, including GE Healthcare and Siemens Healthineers AG, is further supporting market demand for these devices.

Download Free sample to learn more about this report.

Medical Electronics Market Trends

Integration of Technological Advancements to Fuel Product Demand

The integration of technological advancements is emerging as a major trend that is reshaping the global market. The manufacturers are focusing on upgrading diagnostic imaging systems, patient monitoring, and therapeutic devices with artificial intelligence, miniaturized sensors, and software-driven automation. Additionally, improvements in scan speed, image reconstruction, workflow accuracy, and clinical decision support in imaging devices are boosting the demand for these products in the market. In patient monitoring, the shift toward wearable and home-based devices is enabling continuous tracking of vital parameters beyond conventional hospital settings.

Additionally, the integration of precise and digital workflows, especially in surgical electronics, interventional platforms, and life-support therapeutic systems, is resulting in a growing adoption rate for these devices. This shift from standalone hardware to connected, data-enabled devices is enhancing usability, expanding point-of-care applications, and increasing replacement demand for advanced devices across healthcare and homecare settings.

- In August 2025, SAMSUNG, a subsidiary of Samsung Electronics Co., Ltd., launched its next-generation mobile CT product portfolio in India.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Chronic Conditions Cases and Launch of Novel Devices to Drive Market Growth

The growing burden of chronic conditions such as cardiovascular disorders, diabetes, and others is driving the demand for medical electronics devices in the market.

- For instance, according to 2025 data published by the International Diabetes Federation (IDF), it was reported that about 590 million people have diabetes globally.

This, along with increasing healthcare digitalization and the adoption of wearable health devices, is further augmenting the adoption rate of these devices in the market. Therefore, the factors above, along with the growing focus of key players on introducing research and development activities to launch novel devices, are anticipated to boost the adoption rate of these devices, thereby supporting the global market size.

Market Restraints

High Cost Associated with Advanced Equipment to Hamper Market Growth

The high capital cost and total ownership cost of advanced medical electronic equipment are major market restraints limiting the adoption rate, especially in emerging healthcare systems. The large systems, including CT, digital X-ray, MRI, advanced patient monitoring platforms, and surgical electronics, require substantial upfront investment.

Additionally, the cost associated with site preparation, installation, accessories, calibration, and maintenance makes it challenging for hospitals and diagnostic centers to adopt these devices in low- and middle-income countries. Furthermore, expenses related to cybersecurity, software upgrades, and operator training hamper the growth of the market.

- For instance, according to the 2026 statistics published by Block Imaging, Inc., the average cost for a CT scanner ranges from USD 90,000 for basic models to up to USD 900,000 for premium models.

Market Opportunities

Expansion of ASCs in Developing Countries Boost Product Adoption in Market

There is an ongoing expansion of healthcare facilities in developing countries, including India, Mexico, and others. The increasing prevalence of chronic conditions, expansion of healthcare infrastructure, and rising number of ambulatory surgical centers are consequently boosting the adoption of medical electronics in clinical facilities. The preference for ambulatory surgical centers has increased for diagnostic and treatment procedures due to their advantages, including shorter patient stays, faster turnover times, lower procedural costs, and reduced risk of hospital-acquired infections.

- According to 2025 statistics published by Definitive Healthcare, there are about 10,000 active ambulatory surgical centers in the U.S.

Market Challenges

Limited Healthcare Access in Emerging Nations to Restrict Market Growth

There is a growing demand for diagnostic and treatment procedures among the patient population. However, limited availability of technologically advanced devices, limited healthcare spending, along with an inadequate reimbursement framework, particularly in developing nations, are resulting in limited access to healthcare facilities among the patient population.

Moreover, a limited number of healthcare facilities and limited healthcare providers, among others, are some of the crucial factors, resulting in the delayed diagnostic and treatment procedures among the patient population, especially in emerging countries, including India, Mexico, among others.

- For instance, according to 2023 data published by the World Bank Group (WBG), about 4.5 billion people lack full access to essential health services globally.

Other Prominent Challenges

- Strict regulatory requirements to hamper the market growth.

- Data Security Concerns and integration complexity to limit the market growth.

SEGMENTATION ANALYSIS

By Product Type

Increasing prevalence of Chronic Conditions Led to Diagnostic Imaging Devices Segment Dominance

Based on the product type, the market is classified into diagnostic imaging devices, patient monitoring devices, and therapeutic devices. Diagnostic imaging devices are further classified into MRI, X-ray, CT, IVD analyzers, and others. Additionally, patient monitoring devices are segmented into blood glucose monitors, cardiac monitors, hemodynamic monitors, and others. Furthermore, therapeutic devices are divided into surgical & operating room electronics, life support devices, and others.

The diagnostic imaging devices segment held the largest revenue share in 2025. The growth is due to the increasing prevalence of chronic conditions, such as cancer, among the patient population, resulting in a rising number of diagnostic imaging procedures globally. This, along with the increasing focus of key players on launching innovative devices, is further anticipated to contribute to the global medical electronics market growth.

- For instance, according to 2026 statistics published by the American Cancer Society, approximately 2.1 million new cancer cases are projected to occur in the U.S.

The patient monitoring devices segment is expected to grow at a CAGR of 5.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Increasing Launches of Products with Advanced Sensors Led to Dominance of Sensors Segment

Based on component, the market is segmented into sensors, microprocessors/microcontrollers, memory devices, and others.

The sensors segment dominated the global market in 2025 and accounted for a share of 41.9%. The growth is due to the increasing demand for innovative patient monitoring products, resulting in growing R&D activities among the key players to launch novel products with advanced sensors. Thereby, supporting the adoption rate of these devices in the market.

- For instance, in December 2025, Medtronic, a player in healthcare technology, launched the MiniMed 780G system integrated with the Instinct sensor, made by Abbott and designed exclusively for MiniMed systems.

The segment of microprocessors/microcontrollers is set to flourish with a growth rate of 5.3% across the forecast period.

By End User

Increasing Number of Hospitals & ASCs Led to Segmental Dominance

Based on end user, the market is classified into hospitals & ASCs, specialty clinics, diagnostic laboratories, and others.

The hospitals & ASCs segment dominated the market in 2025. The increasing prevalence of chronic diseases, rising number of patient admissions in hospitals, and growing number of hospitals, are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 60.6% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, specialty clinics in the end user segment are projected to grow at a 5.6% CAGR during the forecast period.

Medical Electronics Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Electronics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 3.92 billion, and also took the leading share in 2025 with USD 4.11 billion. The growing prevalence of chronic diseases, advanced hospital infrastructure, and growing launches for advanced medical devices, such as implantable devices, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 statistics published by the Center for Disease Control & Prevention (CDC), the prevalence of Inflammatory Bowel Disease (IBD) is estimated between 2.4 and 3.1 million among patients in the U.S.

U.S. Medical Electronics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.77 billion in 2026, accounting for roughly 33.4% of global sales.

Europe

Europe is projected to record a growth rate of 4.3% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.06 billion by 2026. The strong medical device manufacturing sector and strong preference for home healthcare treatment options are anticipated to support the market growth.

U.K. Medical Electronics Market

The U.K. market in 2026 is estimated at around USD 0.36 billion, representing roughly 3.2% of global revenues.

Germany Medical Electronics Market

Germany’s market is projected to reach approximately USD 0.73 billion in 2026, equivalent to around 6.5% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 2.99 billion in 2026 and secure the position of the third-largest region in the market. The fastest growth in diagnostic and treatment procedures, increasing healthcare investment, among others, is mostly to support the growth of the market.

Japan Medical Electronics Market

The Japan market in 2026 is estimated at around USD 0.52 billion, accounting for roughly 4.6% of global revenues. Japan has historically reported a relatively high prevalence of chronic conditions, with a large number of hospital admissions.

China Medical Electronics Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.89 billion, representing roughly 7.9% of global sales.

India Medical Electronics Market

The Indian market size in 2026 is estimated at around USD 0.39 billion, accounting for roughly 3.5% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.51 billion in 2026. The growth is driven by increasing adoption of medical equipment in the region. The Middle East & Africa are also expected to grow due to emerging healthcare infrastructure development in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.18 billion in 2026.

South Africa Medical Electronics Market

The South Africa market value is projected to reach around USD 0.07 billion in 2026, representing roughly 0.6% of global revenues.

Competitive Landscape

Key Industry Players

Expansion of Geographical Presence to Support Dominance of Key Players in Market

A strong and wide-ranging device portfolio, combined with a notable focus on inorganic expansion strategies worldwide, is a key factor driving the market leadership of these companies. GE HealthCare and Siemens Healthineers AG are among the leading players in 2025. Furthermore, the increasing emphasis of major companies on scaling manufacturing capacities in emerging economies is expected to enhance their market presence and boost their global medical electronics market share.

- In July 2024, Siemens Healthineers AG announced the manufacturing of the Multix Impact E digital radiography X-ray machine in India.

Additionally, other companies, including Medtronic, are also expanding their footprint in the market, largely driven by their increasing focus on mergers, acquisitions, and strategic partnerships to reinforce their position.

List of Key Medical Electronics Companies Profiled

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Medtronic (Ireland)

- Abbott (U.S.)

- Baxter (U.S.)

- Stryker (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM CORPORATION (Japan)

- Koninklijke Philips N.V. (Netherlands)

- Boston Scientific Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Stryker, a global player in medical technologies, launched the next generation of SurgiCount+ within its sponge management portfolio with an aim to strengthen its device channel.

- November 2024: Abbott established a new manufacturing facility with an aim to expand its geographical presence in Kilkenny, Ireland.

- October 2024: Boston Scientific Corporation received U.S. FDA approval for the navigation-enabled FARAWAVE NAV Ablation Catheter for the treatment of paroxysmal atrial fibrillation (AF) and FDA 510(k) clearance for the new FARAVIEW Software, to provide visualization for cardiac ablation procedures with the FARAPULSE Pulsed Field Ablation (PFA) System.

- April 2024: GE HealthCare launched the Voluson Signature 20 and 18 ultrasound systems, which comprehensively integrate Artificial Intelligence (AI), advanced tools, and an ergonomic design to speed exam time for clinicians.

- April 2024: GE HealthCare introduced Caption AI on Vscan Air SL with an aim to expand access to cardiac care.

- April 2024: Koninklijke Philips N.V., announced a strategic partnership to integrate smartQare’s advanced solution, viQtor, with the company’s clinical patient monitoring platforms. This collaboration aims to enable the next generation of continuous patient monitoring across healthcare settings in Europe.

- January 2024: Siemens Healthineers AG launched the Naeotom Alpha class, including a second dual-source scanner, Naeotom Alpha.Pro. with an aim to strengthen its device channel.

REPORT COVERAGE

The global medical electronics market report provides a detailed analysis and focuses on key aspects such as leading companies and market segmentation, including product type, component, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Component, End User, and Region |

| By Product Type |

|

| By Component |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 10.68 billion in 2025 and is projected to reach USD 16.73 billion by 2034.

In 2025, the market value stood at USD 4.11 billion.

Growing at a CAGR of 5.1%, the market will exhibit steady growth over the forecast period.

By product type, the diagnostic imaging devices segment is the leading segment in this market.

The introduction of novel medical electronics is one of the major factors driving the markets growth.

GE HealthCare and Siemens Healthineers AG are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic diseases, the increasing number of diagnostic and treatment procedures, are some of the crucial factors anticipated to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us