Green Logistics Market Size, Share & Industry Analysis, By Mode of Transportation (Road Transportation, Freight {Rail, Sea, Air}, & Intermodal Transportation), By Service Type (Green Transportation Services, Green Warehousing, Reverse Logistics, Others), By End-Use Industry (Retail, Manufacturing, Healthcare, & FMCG), By Technology Adoption (Electric Fuel Vehicles, AI & Route Optimization Software, IoT & Smart Tracking Systems), By Business Model (In-house Sustainable Logistics Operations, 3PL & 4PL Green Services, & Digital Freight Platforms), and Regional Forecast, 2026 - 2034

Green Logistics Market Size and Future Outlook

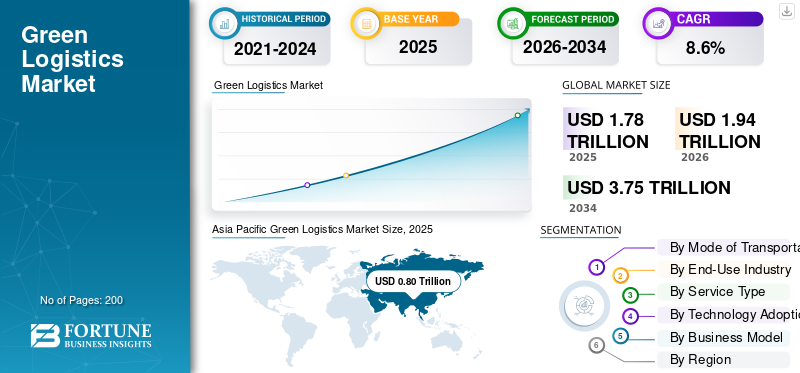

The global green logistics market size was valued at USD 1.78 trillion in 2025. The market is projected to grow from USD 1.94 trillion in 2026 to USD 3.75 trillion by 2034, exhibiting a CAGR of 8.6% during the forecast period. Asia Pacific dominated the green logistics market with a market share of 44.94% in 2025.

Green logistics refers to environmentally sustainable transportation, warehousing, and supply chain practices focused on reducing carbon emissions, improving energy efficiency, minimizing waste, and promoting eco-friendly technologies to support responsible and low-impact goods movement. The market growth is driven by stringent emission regulations, rising corporate ESG commitments, expanding e-commerce demand, fleet electrification, renewable-powered warehousing, digital route optimization, and increasing investments in low-carbon transportation infrastructure globally.

Major players in the market include DHL Group, UPS, FedEx, DB Schenker, Maersk, and XPO Logistics. These companies are competing through fleet electrification, carbon tracking platforms, sustainable warehousing, AI-driven route optimization, and low-emission transportation solutions.

Download Free sample to learn more about this report.

GREEN LOGISTICS MARKET TRENDS

Accelerating Electrification and Alternative Fuel Adoption Reshaping Logistics Operations

One of the major market trends is the rapid adoption of electric vehicles (EVs), hydrogen fuel cell trucks, and biofuel-powered fleets. Logistics providers are increasingly investing in low-emission transportation solutions to align with corporate sustainability targets and evolving regulatory frameworks. Fleet electrification, combined with renewable-powered warehouses, is transforming supply chain networks. This shift is significantly influencing market trends, enhancing brand positioning, and contributing to long term market growth across developed and emerging economies.

- In January 2026, Maersk began deploying state-of-the-art Volvo electric trucks across 14 countries to cut logistics CO₂ emissions and support decarbonization of road freight operations, despite higher upfront costs and longer charging times, aligning with its net-zero by 2040 target while helping customers reduce Scope 1-3 emissions through scalable EV trucking solutions.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Environmental Regulations and Corporate Sustainability Goals to Drive Market Expansion

Government mandates on carbon emissions, fuel consumption efficiency standards, and reporting transparency are key drivers accelerating the product adoption. Policies such as carbon taxation, emission caps, and sustainable procurement requirements are compelling companies to transition toward eco-friendly transportation and warehousing practices. Additionally, multinational corporations are integrating ESG commitments into supply chains, boosting investment in renewable energy and sustainable logistics infrastructure. These regulatory and corporate pressures are poised to strongly support green logistics market growth during the forecast period.

- In February 2026, New York lawmakers passed the Climate Corporate Data Accountability Act, requiring companies with over USD 1 billion in revenue to annually disclose Scope 1, Scope 2, and Scope 3 greenhouse gas emissions. The phased reporting would begin in 2027 and 2028 to boost climate transparency and regulatory oversight.

MARKET RESTRAINTS

High Initial Capital Investment to Limit Rapid Adoption of Green Infrastructure

Despite strong market growth potential, the substantial upfront costs associated with fleet electrification, charging infrastructure, warehouse automation, and renewable energy integration remain a major restraint. Small and medium-sized logistics providers often face financial constraints when transitioning from conventional operations to sustainable alternatives. The higher acquisition cost of electric trucks and advanced digital systems slows adoption, particularly in developing regions. This financial barrier impacts overall product demand and delays uniform market penetration.

MARKET OPPORTUNITIES

Rising E-Commerce Expansion to Create Opportunities for Sustainable Last-Mile Delivery

The continuous expansion of e-commerce platforms is creating significant opportunities for green logistics providers. Growing parcel volumes and urban delivery networks are encouraging the adoption of electric vans, cargo bikes, and AI-enabled route optimization for efficient last- mile delivery operations. Consumers increasingly prefer environmentally responsible delivery options, strengthening the demand for low-emission logistics services. This evolving consumer behavior presents strong market growth prospects and expands market share for companies offering sustainable solutions.

- In February 2026, DHL Group and JD.com signed a memorandum of understanding in Beijing to support German brands’ expansion into China and Europe, leveraging DHL’s global logistics network and JD.com’s e-commerce platforms to provide integrated cross-border fulfilment, preferential import schemes, and market access for seamless supply chain solutions.

MARKET CHALLENGES

Infrastructure Gaps and Limited Charging Networks to Challenge Scalable Deployment

A key challenge in the market is the uneven availability of charging and alternative fuel infrastructure across various regions. Limited public charging networks, grid capacity constraints, and inconsistent hydrogen refueling facilities hinder large-scale fleet deployment. Logistics operators must carefully plan routes and operations around infrastructure limitations, increasing operational complexity. These constraints create uncertainty during the forecast period and require coordinated public-private investments to ensure sustainable and scalable market growth.

Segmentation Analysis

By Mode of Transportation

Expanding Global Trade Volumes and Cost Efficiency to Strengthen Sea Freight Segment Leadership

Based on the mode of transportation, the market is segmented into road transportation, rail freight, sea freight, air freight, and intermodal transportation.

The sea freight segment dominates the green logistics market share due to its cost efficiency in bulk transportation and lower carbon emissions per ton-kilometer compared to air freight. Growing international trade volumes, containerization, and the adoption of cleaner marine fuels such as LNG and biofuels support sustained market growth. Shipping companies are increasingly investing in energy-efficient vessels and digital route optimization, strengthening long-term market demand and market share.

The air freight segment is projected to expand at a CAGR of 10.9% during the forecast period. Rising cross-border e-commerce, demand for time-sensitive deliveries, and investments in sustainable aviation fuel (SAF) and carbon offset programs are accelerating green transformation in air cargo operations.

- In February 2026, DSV unveiled a comprehensive decarbonization roadmap to reduce logistics emissions across road, sea, and air, targeting net-zero by 2050 with interim cuts of 50% for Scope 1/2 and 30% for Scope 3 by 2030. The roadmap highlights the deployment of sustainable aviation fuel, biofuels, and expanded renewable energy in warehouses and fleets to support cleaner transport operations and customer supply chain decarbonization efforts.

By End-Use Industry

Strong Industrial Supply Chains and Bulk Freight Movement to Reinforce Manufacturing & Industrial Segment Dominance

Based on end-use industry, the market is segmented into retail & e-commerce, manufacturing & industrial, automotive, healthcare & pharmaceuticals, and FMCG.

The manufacturing & industrial segment holds the largest share in the market due to high-volume raw material movement, bulk cargo transportation, and globalized production networks. Large-scale industrial operations require integrated multimodal logistics solutions, sustainable warehousing, and fuel-efficient freight systems. The increasing adoption of carbon reporting frameworks and energy-efficient fleet management further supports steady market growth and long-term market demand across industrial supply chains.

The retail & e-commerce segment is projected to expand at a CAGR of 10.4% during the forecast period. Rapid online shopping growth, same-day delivery expectations, and rising adoption of electric last-mile fleets are accelerating sustainable logistics investments within this segment.

- In November 2025, China launched a national green eco-friendly packaging initiative for e-commerce, promoting recyclable materials, reducing plastic usage, standardized parcel sizing, and digital tracking systems to cut packaging waste and lower carbon emissions across high-volume online retail and e-commerce logistics networks.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Fleet Electrification and Low-Emission Freight Solutions to Drive Green Transportation Services Demand

Based on service type, the market is segmented into green transportation services, green warehousing, green packaging solutions, reverse logistics, and carbon management & consulting services.

The green transportation services segment dominates the market as transportation accounts for the largest share of supply chain emissions. Companies are prioritizing fleet electrification, alternative fuels, AI-based route optimization, and fuel-efficient freight systems to reduce carbon intensity. Strong regulatory mandates and corporate decarbonization commitments are accelerating investments in sustainable transport solutions, supporting consistent growth and expanding market share across global logistics networks.

The carbon management & consulting services segment is projected to grow at a CAGR of 11.9% during the forecast period. Rising ESG compliance requirements, mandatory emissions reporting, and science-based net-zero targets are driving increased demand for carbon tracking, auditing, and sustainability advisory services.

- In February 2026, Hapag-Lloyd and DSV expanded their decarbonization partnership through an agreement covering 18,000 tonnes of carbon-reduced ocean transport using advanced biofuels. The move would enable significant Scope 3 emission reductions and supporting low-emission maritime freight operations across global trade lanes.

By Technology Adoption

Large-Scale Fleet Electrification Initiatives to Impel Electric & Alternative Fuel Vehicles Segment Growth

Based on technology adoption, the market is segmented into electric & alternative fuel vehicles, AI & route optimization software, warehouse automation & energy management systems, IoT & smart tracking systems, and carbon tracking & reporting platforms.

The electric & alternative fuel vehicles segment holds the dominating share as transportation decarbonization remains the primary focus for logistics providers. Companies are increasingly deploying battery electric trucks, hydrogen fuel cell vehicles, and biofuel-powered fleets to comply with emission regulations and corporate sustainability targets. Government incentives, declining battery costs, and infrastructure expansion further strengthen market growth and long-term market demand.

- In November 2025, Amazon Freight outlined plans at the White Label World Expo to transform retail transportation toward sustainability by leveraging electric and low-emission vehicles, AI-driven route optimization, and integrated load-planning systems. The move was aimed at reducing energy consumption and carbon emissions across last-mile and long-haul networks while enhancing delivery reliability and cost efficiency for retail partners.

The carbon tracking & reporting platforms segment is projected to expand at a CAGR of 10.3% during the forecast period. Growing regulatory disclosure requirements, Scope 3 emissions monitoring, and ESG transparency initiatives are accelerating the adoption of advanced digital carbon accounting and analytics solutions.

By Business Model

Integrated Service Capabilities and Global Network Expansion to Strengthen 3PL Green Services Market

Based on business model, the market is segmented into in-house sustainable logistics operations, third-party logistics (3PL) green services, fourth-party logistics (4PL) sustainable integrators, asset-based green logistics providers, and non-asset-based/digital freight platforms.

The third-party logistics (3PL) green services segment holds the largest market share due to its integrated transportation, warehousing, and sustainability expertise. Large enterprises increasingly outsource logistics to specialized 3PL providers offering fleet electrification, carbon reporting, and multimodal optimization. Established global networks, scalable infrastructure, and advanced digital platforms enable 3PLs to drive consistent market growth and capture significant market demand.

The non-asset-based/digital freight platforms segment is projected to grow at a CAGR of 11.5% during the forecast period. Rising adoption of AI-driven freight matching, real-time emissions tracking, and asset-light digital brokerage models is accelerating platform-based green logistics solutions.

- In December 2025, Zero Carbon Freight announced progress on its Digital Spine platform, integrating real-time freight data, standardized carbon measurement tools, and interoperable digital systems to accelerate emissions tracking, improve supply chain transparency, and support scalable low-carbon freight operations across U.K. logistics networks.

Green Logistics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Green Logistics Market Size, 2025 (USD Trillion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific leads the market and is projected to register the fastest CAGR during the forecast period. Rapid industrialization, expanding e-commerce volumes, and strong export-oriented manufacturing hubs in China, India, Japan, and Southeast Asia are accelerating market demand. Government incentives for electric commercial vehicles, investments in smart ports, and renewable-powered warehousing are strengthening market growth. Increasing regulatory focus on emission reduction and digital freight platforms further supports the expansion of the regional market share.

- In February 2026, DHL Group announced new sustainability milestones in the Asia Pacific, expanding electric vehicle fleets, increasing the use of sustainable aviation fuel, and scaling carbon-neutral warehousing solutions to reduce emissions and strengthen low-carbon supply chain operations across key regional markets.

China Green Logistics Market

The China market is estimated to touch around USD 0.41 trillion in 2026, accounting for roughly 21.3% of global market revenues. Strong manufacturing exports, large-scale fleet electrification, smart port investments, and government-backed decarbonization policies drive sustained market growth and regional dominance.

Japan Green Logistics Market

The Japan market is estimated to reach around USD 0.10 trillion in 2026, accounting for roughly 5.0% of global market revenues. Advanced automation, hydrogen-powered transport pilots, carbon neutrality commitments, and efficient urban freight systems support stable market demand and technological leadership.

India Green Logistics Market

The India market is estimated to reach around USD 0.09 trillion in 2026, accounting for roughly 4.8% of global market revenues. Rapid e-commerce expansion, infrastructure modernization, EV adoption incentives, and dedicated freight corridors are accelerating market growth at the fastest pace regionally.

Europe

Europe holds the second-largest market share and is expected to grow at a CAGR of 8.7% during the forecast period. Strict carbon regulations, the EU Green Deal, and sustainable transport mandates are major drivers of market growth. High adoption of electric trucks, rail freight electrification, and sustainable aviation fuel initiatives strengthen market demand. Advanced carbon tracking frameworks and corporate ESG commitments further support long-term market trends.

- In January 2026, IFA Forwarding highlighted Europe’s accelerating green logistics transition, driven by EU climate regulations, multimodal freight expansion, electric truck adoption, rail electrification, and sustainable warehousing initiatives aimed at reducing transport emissions and improving supply chain efficiency.

Germany Green Logistics Market

The Germany market is estimated to touch around USD 0.09 trillion in 2026, accounting for roughly 4.5% of the global market revenues. Strong industrial exports, rail freight electrification, strict emission regulations, and ESG-driven corporate investments are reinforcing sustainable supply chain transformation.

U.K. Green Logistics Market

The U.K. market is estimated to reach around USD 0.07 trillion in 2026, accounting for roughly 3.5% of the global market revenues. Net-zero targets, sustainable aviation fuel initiatives, urban EV fleets, and digital freight platforms are supporting steady market growth.

North America

North America represents the third-largest market, driven by corporate decarbonization targets and federal clean transportation incentives. The U.S. and Canada are witnessing increased adoption of electric delivery fleets, intermodal rail solutions, and green warehousing technologies. Growth in cross-border trade and e-commerce supports steady market demand. While infrastructure expansion is ongoing, private-sector investments and carbon reporting regulations are gradually enhancing market growth and competitive market share positioning.

- In October 2024, DHL Supply Chain and Diageo North America began operating Nikola hydrogen fuel cell trucks in the U.S., featuring zero tailpipe emissions and extended driving range, supporting sustainable freight transportation and reducing carbon intensity across beverage distribution networks.

U.S. Green Logistics Market

The U.S. market is estimated to touch a value of around USD 0.35 trillion in 2026, accounting for roughly 17.9% of global market revenues. Federal clean transport incentives, large-scale electric truck deployment, intermodal freight expansion, and corporate sustainability commitments drive strong market demand.

Rest of the World

The market in the rest of the world is experiencing gradual growth in the market, supported by infrastructure modernization and expanding trade corridors in South America, the Middle East, and Africa. Governments are increasingly promoting renewable energy integration and sustainable transport policies. Although adoption remains at an early stage compared to developed markets, rising foreign investments, port electrification projects, and logistics digitalization initiatives are contributing to improving market demand and long-term market growth potential.

- In September 2025, UAE regulators emphasized strengthened green finance frameworks and sustainability-linked regulations to boost investor confidence, supporting low-carbon infrastructure, renewable energy projects, and environmentally responsible logistics development aligned with national net-zero commitments.

COMPETITIVE LANDSCAPE

Key Industry Players

Decarbonization Strategies, Digital Freight Platforms, and Global Network Expansion Define Competitive Intensity

The market is moderately fragmented, with global logistics giants and regional specialists competing on sustainability, scale, and digital capabilities. Key players such as DHL Group, UPS, FedEx, DB Schenker, Maersk, and XPO Logistics focus on fleet electrification, sustainable fuels, AI-driven route optimization, and carbon tracking platforms. Companies strengthen competitiveness through green warehousing, multimodal integration, and ESG-aligned service offerings. Strategic partnerships, renewable energy investments, and technology acquisitions support market share expansion.

- In December 2025, DHL deployed its initial eight battery-electric heavy-duty trucks under the Hylane rental agreement, supporting zero-emission freight operations in Germany, reducing CO2 emissions, and advancing scalable electric long-haul transportation within its decarbonization roadmap.

LIST OF KEY GREEN LOGISTICS COMPANIES PROFILED

- DHL Group (Germany)

- United Parcel Service (UPS) (U.S.)

- FedEx Corporation (U.S.)

- DB Schenker (Germany)

- P. Moller–Maersk (Denmark)

- Kuehne+Nagel (Switzerland)

- DSV A/S (Denmark)

- CEVA Logistics (France)

- Nippon Express Holdings (Japan)

- XPO, Inc. (U.S.)

- H. Robinson Worldwide, Inc. (U.S.)

- Expeditors International of Washington, Inc. (U.S.)

- CMA CGM Group (France)

- Deutsche Post DHL Supply Chain (Germany)

- Lineage Logistics (U.S.)

- Agility Public Warehousing Company KSCP (Kuwait)

KEY INDUSTRY DEVELOPMENTS

- November 2025: The e-Dutra Coalition was launched in Brazil to accelerate freight electrification along the Presidente Dutra highway corridor, promoting heavy-duty electric truck deployment, charging infrastructure expansion, and collaborative public-private initiatives to reduce transport emissions and modernize national logistics mobility.

- September 2025: Echo Global Logistics was named an Inbound Logistics Green Supply Chain Partner for advancing sustainable freight solutions, including multimodal optimization, carrier emissions tracking, and data-driven route efficiency programs that help shippers reduce transportation-related carbon footprints.

- November 2024: Cainiao unveiled green logistics innovations at COP29, announcing annual carbon reductions of 458,000 tons through smart routing algorithms, renewable-powered warehouses, electric delivery fleets, and recyclable packaging solutions across its global e-commerce logistics network.

- October 2024: The Green Finance Platform published research on unlocking green logistics development, highlighting blended finance models, sustainability-linked loans, carbon pricing mechanisms, and public-private investment frameworks to accelerate low-emission transport infrastructure and sustainable supply chain transformation globally.

- August 2024: SHL Medical partnered with global logistics providers to launch a green logistics initiative integrating sustainable aviation fuel, optimized cold-chain transport, and carbon monitoring systems for reducing emissions across temperature-controlled pharmaceutical supply chains and strengthen ESG commitments.

- July 2024: DHL and Envision launched a green logistics partnership integrating renewable energy solutions, battery storage systems, and digital energy management platforms to decarbonize transportation and warehousing operations, supporting net-zero supply chain objectives through scalable clean energy deployment.

- January 2022: DSV launched an expanded Green Logistics service portfolio focused on sustainable aviation fuel, biofuel-based ocean freight, electric road transport, and carbon reporting tools, enabling customers to reduce Scope 1, 2, and 3 emissions while accelerating supply chain decarbonization.

REPORT COVERAGE

The global green logistics market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.6% from 2026-2034 |

| Unit | Value (USD Trillion) |

| Segmentation | By Mode of Transportation, By End-Use Industry, By Service Type, By Technology Adoption, By Business Model, and By Region |

| By Mode of Transportation |

|

| By End-Use Industry |

|

| By Service Type |

|

| By Technology Adoption |

|

| By Business Model |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.78 trillion in 2025 and is projected to reach USD 3.75 trillion by 2034.

In 2025, the Asia Pacific market value stood at USD 0.80 trillion.

The market is expected to exhibit a CAGR of 8.6% during the forecast period of 2026-2034.

The sea freight segment leads the market in terms of mode of transportation.

Stringent environmental regulations and corporate sustainability goals are key factors driving the market.

Key players in the market include DHL Group, UPS, FedEx, DB Schenker, Maersk, and XPO Logistics.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us