Agriculture Chemical Packaging Market Size, Share & Industry Analysis, By Material (Plastics, Metal, Paper & Paperboard, Glass, and Others), By Packaging Type (Bottles, Bags & Sacks, Pouches, Intermediate Bulk Containers (IBCs), Drums & Jerry Cans, and Others), By Chemical Type (Pesticides, Fertilizers, Plant Growth Regulators, Bio-stimulants, and Others), and Regional Forecast, 2026-2034

Agriculture Chemical Packaging Market Size and Future Outlook

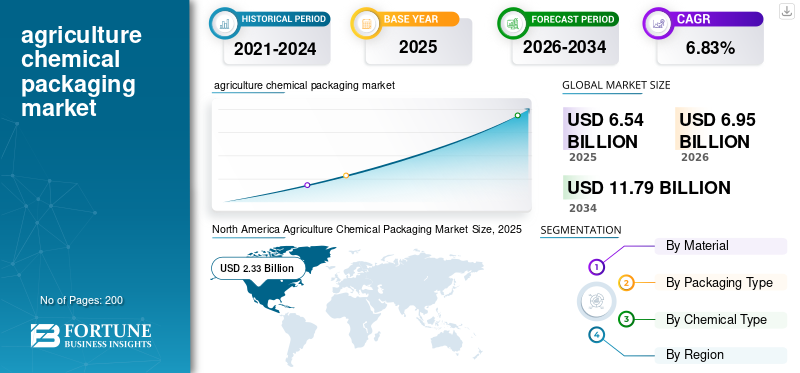

The global agriculture chemical packaging market size was valued at USD 6.54 billion in 2025. The market is projected to grow from USD 6.95 billion in 2026 to USD 11.79 billion by 2034, exhibiting a CAGR of 6.83% during the forecast period. North America dominated the agriculture chemical packaging market with a market share of 35.62% in 2025.

The global sector comprises the industry that creates, manufactures, and distributes packaging solutions for the storage, transportation, and dispensing of agrochemicals, including pesticides, herbicides, fungicides, and fertilizers. The growing global demand for food and the increased use of crop protection chemicals are driving the need for robust, safe, leak proof, and compliant packaging solutions, particularly in developing agricultural economies.

Furthermore, many key industry players, such as Amcor, Greif Inc., and Mauser Packaging Solutions, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

AGRICULTURE CHEMICAL PACKAGING MARKET TRENDS

Shift Toward Sustainable and Eco-Friendly Packaging is a Prominent Trend Observed in Market

A significant trend in the global sector is the growing shift toward sustainable, environmentally friendly packaging options. Innovations such as mono-material plastics, reusable containers, and minimized resin packaging are becoming more popular among agrochemical firms. Furthermore, there is a growing focus on circular-economy initiatives that encompass container collection and recycling programs. This trend is additionally reinforced by a growing awareness among farmers and distributors about environmental safety. Consequently, companies are allocating resources to research and development to create packaging that harmonizes durability, chemical resistance, and sustainability.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Agrochemicals is Driving Market Growth

The main factor driving the global agriculture chemical packaging market growth is the rising demand for agrochemicals, fueled by the need to improve crop productivity. As the global population continues to grow, the agricultural sector faces substantial pressure to increase yields from a limited amount of arable land. This situation has led to increased use of pesticides, herbicides, and fertilizers, all of which require specialized packaging solutions for secure storage and transportation. Moreover, the growth of commercial farming and the adoption of modern agricultural practices, especially in developing regions, are increasing the consumption of agrochemicals.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Stringent Regulatory Requirements Hampers Market Growth

Strict regulatory standards governing the storage, transportation, and disposal of agrochemical packaging pose a significant barrier to market expansion. Government bodies and environmental organizations enforce rigorous guidelines to guarantee the safe management of hazardous substances and to reduce environmental pollution. Adhering to these regulations often requires substantial investment in sophisticated raw materials, testing, labeling, and certification, thereby increasing overall production costs. Smaller packaging firms, especially, may encounter difficulties in fulfilling these requirements, which can limit market access and impede innovation in affordable packaging alternatives.

MARKET OPPORTUNITIES

Growth in Emerging Agricultural Economies Offers Potential Growth Opportunities

The rise of agricultural economies offers a considerable opportunity for the sector. Nations in Asia Pacific, Latin America, and Africa are undergoing rapid agricultural advances, bolstered by government support, improved farming practices, and growing investments in agrochemicals. Furthermore, the expansion of agrochemical distribution networks and retail outlets is driving increased demand for various packaging formats. Packaging manufacturers can leverage this opportunity by providing economical, robust, and regionally tailored solutions that meet local climate conditions and regulatory standards.

MARKET CHALLENGES

Safe Disposal and Recycling of Chemical Packaging Waste Pose a Critical Challenge to Market Growth

A significant challenge within the global market is the secure disposal and recycling of utilized packaging materials. In many areas, particularly in developing nations, inadequate collection and recycling infrastructure exacerbates the problem. Inadequate disposal methods can result in soil and water pollution, which poses threats to human health and ecosystems. Tackling this issue necessitates collaborative efforts from manufacturers, governmental bodies, and end users to establish efficient take-back programs, recycling systems, and educational initiatives.

Segmentation Analysis

By Material

Versatility, Cost Efficiency, and Regulatory Compliance Drive Dominance of Plastic Segment

Based on the material, the market is divided into plastics, metal, paper & paperboard, glass, and others.

The plastic segment is expected to account for the largest share of the market. Plastic materials are the leading choice in the global market, primarily due to their cost-effective durability and chemical resistance. Their lightweight characteristics help to lower logistics expenses and enhance handling efficiency throughout the supply chain. Moreover, plastics can be easily shaped into various forms, such as bottles, cans, drums, and intermediate bulk containers, allowing customization to meet product specifications. Compared with alternatives such as metal or glass, plastics offer superior impact resistance and a reduced risk of breakage, making them particularly appropriate for agricultural settings.

The paper and paperboard segment is expected to grow at a CAGR of 6.62% over the forecast period.

By Packaging Type

Ease of Handling, Precise Dispensing, and Wide Applicability Drive Dominance of Bottles Segment

Based on packaging type, the market is segmented into bottles, bags & sacks, pouches, Intermediate Bulk Containers (IBCs), drums & jerry cans, and others.

In 2025, the bottles segment dominates the market. The segment of bottle packaging types leads the global market owing to its ease of handling, accurate dispensing features, and compatibility with a diverse array of agrochemical products. Furthermore, bottles can accommodate various closure systems, including measuring caps and tamper-evident seals, which improve safety and regulatory compliance. They are also economical and versatile, made from different materials such as HDPE, making them suitable for packaging liquid pesticides, herbicides, and fertilizers.

The bags and sacks segment is projected to grow at a CAGR of 6.91% over the forecast period.

By Chemical Type

To know how our report can help streamline your business, Speak to Analyst

High Usage Volume, Crop Protection Necessity, and Frequent Application Drive Dominance of Pesticides Segment

Based on the chemical type, the market is segmented into pesticides, fertilizers, plant growth regulators, bio-stimulants, and others.

The pesticides segment is expected to hold a dominant agriculture chemical packaging market share over the forecast period. The pesticides sector leads the global market owing to its widespread use and its essential role in safeguarding crops against pests, insects, and diseases. The rising demand to reduce crop losses and enhance agricultural efficiency has led to a surge in pesticide use, especially in areas with intensive farming methods. Moreover, stringent safety and handling regulations for hazardous materials require specific packaging types, such as sealed bottles and containers, thereby increasing the need for packaging solutions designed specifically for pesticide products.

The fertilizers segment is projected to grow at a CAGR of 6.22% over the forecast period.

Agriculture Chemical Packaging Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Agriculture Chemical Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 2.20 billion, and maintained its leading position in 2025, at USD 2.33 billion. Sophisticated agricultural techniques, widespread implementation of precision farming, and stringent regulations regarding chemical management propel the market. Demand is shaped by the need for sustainable, recyclable packaging, coupled with the growing use of high-value crop protection chemicals that require specialized, high-performance packaging solutions.

U.S. Agriculture Chemical Packaging Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 1.85 billion in 2025, accounting for roughly 28.26% of global sales. In the U.S., demand is driven by extensive mechanized agriculture and strict regulations governing the storage and transportation of chemicals. There is a significant emphasis on sustainable packaging solutions, including recyclable and returnable containers, as well as the growing implementation of sophisticated dispensing systems for accurate application.

Asia Pacific

Asia Pacific is estimated to reach USD 1.85 billion in 2025 and secure the position of the second-largest region in the market. The rapid expansion of agriculture, rising food demand, and increased agrochemical use are key factors driving the market in the Asia Pacific region. Additionally, heightened awareness of the safe handling of chemicals and governmental backing for contemporary farming practices further enhance demand for packaging.

Japan Agriculture Chemical Packaging Market

The Japanese market value in 2025 was recorded at around USD 0.35 billion, accounting for roughly 5.30% of global revenues. Cutting-edge agricultural technologies and stringent safety regulations shape Japan's market. The scarcity of arable land necessitates intensive farming practices, thereby increasing dependence on agrochemicals.

China Agriculture Chemical Packaging Market

China's market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 0.59 billion, representing roughly 9.02% of global sales.

India Agriculture Chemical Packaging Market

The Indian market in 2025 was valued at around USD 0.49 billion, accounting for roughly 7.56% of global high-revenue markets.

Europe

Europe is projected to grow at 6.50% over the coming years, the third-highest among regions, and reach a valuation of USD 1.06 billion by 2025. Growth is influenced by rigorous environmental regulations and by circular-economy initiatives. There exists a significant demand for sustainable, reusable, and recyclable packaging solutions. Additionally, the region prioritizes reducing plastic waste, encouraging manufacturers to explore innovative materials while adhering to stringent agrochemical safety standards.

U.K. Agriculture Chemical Packaging Market

The U.K. market size in 2025 was valued at USD 0.20 billion, representing approximately 3.08% of global revenues.

Germany Agriculture Chemical Packaging Market

Germany's market reached approximately USD 0.23 billion in 2025, equivalent to around 3.49% of global sales.

Latin America

The Latin America region is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.85 billion in 2025. The market is propelled by extensive commercial agriculture, especially in nations such as Brazil and Argentina. The widespread use of pesticides and fertilizers in cash crop cultivation increases demand for bulk and intermediate packaging solutions. Additionally, export-focused agriculture requires reliable packaging to ensure product safety during long-distance shipping.

Middle East & Africa

In the Middle East & Africa, South Africa reached USD 0.11 billion in 2025. Growth is facilitated by enhanced agricultural practices and government initiatives to improve food security. The growing use of agrochemicals in arid areas is driving demand for robust, protective packaging.

Saudi Arabia Agriculture Chemical Packaging Market

The Saudi Arabian market reached approximately USD 0.16 billion by 2025, accounting for roughly 2.44% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The global market has a semi-consolidated structure, with prominent players including Amcor, Greif Inc., and Mauser Packaging Solutions. The significant market shares of these packaging companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in September 2024, Amcor announced the expansion of its sustainable packaging range with the introduction of new high-barrier, recyclable HDPE containers tailored specifically for agrochemicals. These containers improve chemical resistance while minimizing environmental impact by utilizing less resin. The company has prioritized improving compatibility with hazardous formulations, thereby ensuring compliance with global safety regulations.

Other notable players in the global market include Schütz GmbH & Co. KGaA, ALPLA Group, and Pyramid Technoplast Ltd. These companies are expected to prioritize new product launches, strategic partnerships, and collaborations to increase their global market shares during the forecast period.

LIST OF KEY AGRICULTURE CHEMICAL PACKAGING COMPANIES PROFILED

- Amcor (Switzerland)

- Greif Inc. (U.S.)

- Mauser Packaging Solutions (U.S.)

- Schütz GmbH & Co. KGaA (Germany)

- ALPLA Group (Austria)

- Pyramid Technoplast Ltd (India)

- Time Technoplast Ltd (India)

- SIG (Switzerland)

- Codefine International SA (Switzerland)

- Black Forest Container Systems LLC (U.S.)

- CurTec Holdings B.V. (Netherlands)

- ProAmpac (U.S.)

- LC Packaging (Netherlands)

- NNZ Group BV (Netherlands)

- Knack Packaging Limited (India)

KEY INDUSTRY DEVELOPMENTS

- July 2024: Greif Inc. has broadened its network for reconditioning Intermediate Bulk Containers (IBCs) throughout North America and Europe. This initiative aids agrochemical manufacturers by facilitating the reuse of industrial packaging, thereby minimizing waste and lowering operational expenses. Greif's improved collection and recycling infrastructure enhances supply chain efficiency while ensuring compliance with stringent hazardous-material-handling regulations.

- June 2024: Mauser Packaging Solutions introduced a new range of sustainable agrochemical packaging as part of its Infinity Series, which includes post-consumer recycled (PCR) materials. These containers are engineered for strength and secure storage of hazardous substances, all while reducing environmental impact. This innovation aligns with regulatory trends and the growing customer demand for environmentally friendly packaging.

- May 2024: Schütz GmbH & Co. KGaA launched an improved ECOBULK IBC system specifically designed for agrochemical uses. This new design includes superior barrier protection and enhanced discharge systems to facilitate the safer handling of liquid pesticides and fertilizers. Additionally, the company has incorporated advanced recycling features, allowing for the reuse of container components.

- April 2024: ALPLA Group has invested to enhance its production capabilities for high-performance plastic containers in the Asia Pacific region. This expansion is focused on the production of lightweight, chemically resistant bottles for agrochemical products. ALPLA's objective is to meet the rising regional demand, driven by growth in agricultural activities and agrochemical consumption.

- March 2024: Time Technoplast Ltd has enhanced its industrial packaging portfolio by boosting the production of composite cylinders and large plastic drums utilized for agrochemicals. This expansion aims to serve both domestic and export markets, with a particular focus on Asia and Africa.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, along with their prevalence by region. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.83% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Packaging Type, Chemical Type, and Region |

| By Material |

|

| By Packaging Type |

|

| By Chemical Type |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.54 billion in 2025 and is projected to reach USD 11.79 billion by 2034.

In 2025, the market value stood at USD 2.33 billion.

The market is expected to grow at a CAGR of 6.83% over the forecast period.

By material, the plastics segment is expected to lead the market.

The increasing demand for agrochemicals is driving market growth.

Amcor, Greif Inc., and Mauser Packaging Solutions are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us