Aerospace Riveting Equipment Market Size, Share & Industry Analysis, By End Use (OEM and MRO), By Equipment (Hydraulic Riveting Equipment, Pneumatic Riveting Equipment, and Electric Riveting Equipment), By Type (Blind Rivet, Semi-Tubular Rivet, and Solid Rivet), By Technology (Automated Riveting Equipment and Manual Riveting Equipment), and Regional Forecast, 2026-2034

Aerospace Riveting Equipment Market Size and Future Outlook

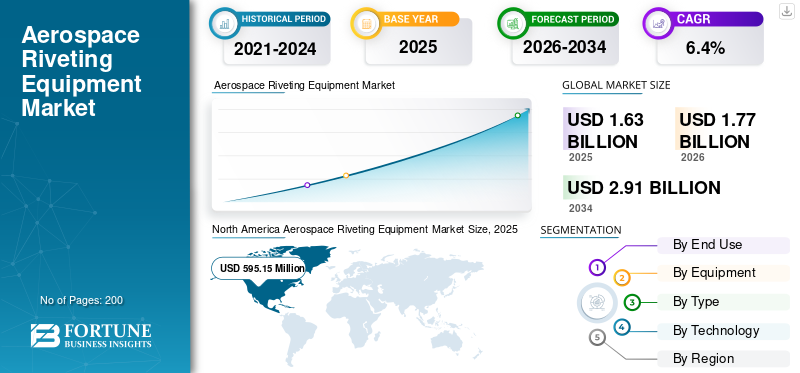

The global aerospace riveting equipment market size was valued at USD 1,631.0 million in 2025. The market is projected to grow from USD 1,774.4 million in 2026 to USD 2,914.1 million by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the aerospace riveting equipment market with a market share of 36.48% in 2025.

The aerospace riveting equipment market encompasses specialized tools and systems for fastening aircraft components, serving OEMs, MRO providers, and defense sectors. It features pneumatic, electric, hydraulic, and robotic solutions tailored for high-precision assembly of fuselages, wings, and structures using metals and composites.

Key players include Airbus Helicopters, Avdel, Boeing Commercial Airplanes, Cherry Aerospace, Eaton Aerospace, GESIPA Aerospace, Henrob, Huck Aerospace, Lockheed Martin, and Northrop Grumman, shaping the market by combining high-reliability fastening tools, production-grade installation systems, automation-ready riveting solutions, and process control.

Download Free sample to learn more about this report.

AEROSPACE RIVETING EQUIPMENT MARKET TRENDS

Shift toward Automation and Lightweight Materials is Shaping Evolution in the Market

The aerospace riveting equipment market is shifting toward automation, robotics, and smart riveting solutions integrated with Industry 4.0 technologies. Manufacturers increasingly adopt these advancements to handle complex aircraft designs and lightweight composites, improving assembly line efficiency and precision. Regional expansion in Asia-Pacific and emerging markets supports this evolution, driven by rising aircraft production and sustainability goals for fuel-efficient structures. Pneumatic and electric tools gain prominence for their versatility in OEM and MRO applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Demand for Lightweight Materials and Precision Assembly Driving Market Growth

Rising emphasis on lightweight materials such as composites and advanced alloys in aircraft construction propels the need for specialized riveting equipment to ensure structural integrity. Increasing aircraft production backlogs and design complexities demand high-precision tools for quality manufacturing. Fleet modernization and air travel recovery further boost the adoption of efficient fastening methods in both commercial and defense sectors.

MARKET RESTRAINTS

High Costs and Regulatory Compliance Hinder the Market Growth

High initial capital for advanced automated systems and ongoing maintenance expenses deter smaller manufacturers from upgrading equipment. Stringent regulatory standards from the FAA and EASA require extensive testing and certification, delaying the introduction of new technologies. Limited adoption of cutting-edge tools due to these financial and compliance barriers slows the global aerospace riveting equipment market growth.

MARKET OPPORTUNITIES

Expansion in Emerging Aerospace Hubs Through Local Investments Curates Market Opportunities

Emerging aerospace hubs in Asia Pacific, Latin America, and the Middle East offer substantial growth potential through local manufacturing investments and fleet expansions. Aftermarket services, including maintenance contracts for aging fleets, provide steady demand for portable and specialized riveting tools. Innovations in materials and joining techniques, alongside partnerships with OEMs including Boeing and Airbus, enable suppliers to capture shares in high-precision assembly needs. Regional diversification mitigates risks from mature markets.

MARKET CHALLENGES

Skilled Workforce Shortages and Cyclical Demand Challenging the Market Growth

Shortages of trained personnel to operate complex automated riveting systems hinder effective deployment and productivity. Dependence on fluctuating aircraft production cycles exposes the market to economic downturns and supply chain issues, as seen in post-pandemic recoveries. High certification hurdles and tariff pressures on parts add layers of difficulty for consistent operations.

Segmentation Analysis

By End Use

Higher Aircraft Build Rates and Line-Rate Commitments Fuel OEM Segment's Growth

Based on end use, the market is bifurcated into OEM and MRO.

The OEM segment is anticipated to account for the largest market share. OEM demand is powered by higher aircraft build rates and line-rate commitments. Manufacturers invest in automated and traceable riveting systems to cut takt time, reduce scrap, and standardize quality across multiple sites.

The MRO (maintenance, repair, and overhaul) segment is anticipated to rise with a CAGR of 5.8% over the forecast period.

By Equipment

Pneumatic Riveting Equipment Segment Dominated Owing to Affordability and Easy Maintenance

Based on equipment, the market is segmented into hydraulic riveting equipment, pneumatic riveting equipment, and electric riveting equipment.

In 2025, the pneumatic riveting equipment segment dominated the global market. Pneumatic riveting demand stays strong because it's proven, affordable, and easy to maintain. It dominates high-frequency shop-floor use, especially in MRO and suppliers where uptime, tool ruggedness, and operator familiarity matter.

The electric riveting equipment segment is projected to grow at a CAGR of 6.8% over the forecast period.

By Type

Solid Rivet Segment Leads the Market Owing to Critical Strength and Fatigue in Primary Structures

Based on type, the market is segmented into blind rivet, semi-tubular rivet, and solid rivet.

The solid rivet segment is anticipated to witness a dominating aerospace riveting equipment market share over the forecast period. Solid rivet demand remains high in primary structures where strength and fatigue performance are critical. Production lines and defense programs sustain volumes, pushing investments in consistent installation, inspection, and rework reduction.

The blind rivet segment is projected to grow at a high CAGR of 6.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Automated Riveting Equipment Segment Led Due to Labor Shortages, Stricter Quality, and Traceability Targets

Based on technology, the market is bifurcated into automated riveting equipment and manual riveting equipment.

The automated riveting equipment segment dominated the market share. Automated riveting demand rises as labor shortages and quality targets intensify. OEMs and tier suppliers deploy robotic and CNC solutions to improve repeatability, integrate inspection, and increase throughput with lower defect rates.

In addition, manual riveting equipment is projected to grow at a CAGR of 6.0% during the forecast period.

Aerospace Riveting Equipment Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Aerospace Riveting Equipment Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 548.57 million, and also maintained the leading share in 2025, with USD 595.15 million. North America's demand is driven by Boeing's production stabilization, defense modernization, and strong tier-supplier ecosystems. Tool upgrades prioritize higher throughput, traceability, and ergonomics, with automation investments expanding across assembly lines and MRO shops.

U.S. Aerospace Riveting Equipment Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 590.6 million in 2026, accounting for roughly 6.2% of global sales. Boeing production needs, major defense programs, and a dense supplier base anchor U.S. demand. Buyers upgrade riveting systems for traceability, repeatability, and automation to reduce labor constraints and defects.

Europe

Europe is estimated to reach USD 509.8 million in 2026 and secure the position of the second-largest region in the market. Europe's demand is supported by Airbus ramp-ups, sustainability-driven process changes, and deep aerostructures supply chains. Manufacturers invest in energy-efficient tooling, quality assurance, and semi-automated riveting to improve cycle times and compliance.

U.K. Aerospace Riveting Equipment Market

The U.K. market in 2026 is estimated at around USD 72.9 million, representing a roughly 6.1% CAGR of global sales. U.K. demand comes from aerostructures manufacturing, engine supply chains, and defense sustainment work. Shops favor ergonomic riveting tools and automated cells that improve consistency, reduce operator fatigue, and support tight certification requirements.

Germany Aerospace Riveting Equipment Market

Germany's market is projected to reach approximately USD 111.1 million in 2026. Airbus-linked manufacturing, advanced composite structures, and precision quality culture shape Germany's demand. Companies invest in automated riveting, process monitoring, and fast tool changeovers to maintain throughput and reduce rework.

Asia Pacific

Asia Pacific is projected to record a growth rate during the forecast period of 7.1%, which is the third highest among all regions, and reach a valuation of USD 456.9 million by 2026. Asia Pacific demand is rising from expanding aircraft assembly, offset work, and growing domestic aerospace programs. Buyers prioritize scalable, cost-effective riveting tools, training-friendly interfaces, and automation pilots to lift productivity and consistency.

Japan Aerospace Riveting Equipment Market

The Japan market share in 2026 is estimated at around USD 82.5 million, accounting for roughly 6.1% of the CAGR during the forecast period. Japan's demand is steady due to high-quality tier manufacturing and strict process control. Firms prefer premium riveting tools, automated systems for repeatability, and data logging that supports compliance and customer auditability.

China Aerospace Riveting Equipment Market

China's market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 177.1 million. China's demand grows with domestic aircraft programs and expanding industrial capacity. Buyers seek robust, scalable riveting equipment, local service support, and semi-automated systems that improve quality while managing labor variability.

India Aerospace Riveting Equipment Market

The Indian market in 2026 is estimated at around USD 65.9 million. India's demand accelerates due to defense indigenization, new aerospace manufacturing parks, and rising MRO capability. Tooling purchases favor cost-effective pneumatic systems today, while automation and electric riveters gain traction quickly.

Rest of the World

The rest of the world includes the Middle East & Africa, and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America markets are set to reach a valuation of USD 99.3 million and USD 61.6 million, respectively in 2026. The rest of the world's demand is led by MRO expansion, airline fleet growth, and localized manufacturing initiatives. Purchases focus on reliable pneumatic tools, portable electric riveters, and inspection-ready processes that cut downtime and rework.

COMPETITIVE LANDSCAPE

Key Industry Players

Demand for High-Throughput and Repeatable Aerospace Riveting Equipment is Driving Market Positioning

Airbus Helicopters and Boeing Commercial Airplanes pull demand through higher production tempo and tighter process control on assembly lines. GESIPA Aerospace pushes battery-powered, operator-friendly blind riveting that reduces corded-tool dependence on the shop floor. Avdel and Huck Aerospace anchor structural fastening with proven installation systems and process know-how that suppliers can standardize globally. Cherry Aerospace strengthens handheld and production tooling for high-cycle riveting environments. Henrob advances forming and joining approaches that help manufacturers control distortion and rework. Eaton Aerospace supports the wider actuation and aerospace tooling ecosystem where reliability and lifecycle service matter. Lockheed Martin and Northrop Grumman accelerate rugged, high-spec riveting solutions aligned to defense programs, where consistency, inspection readiness, and traceability are non-negotiable.

LIST OF KEY AEROSPACE RIVETING EQUIPMENT COMPANIES PROFILED IN REPORT

- Airbus Helicopters (France)

- Avdel (U.K)

- Boeing Commercial Airplanes (U.S.)

- Cherry Aerospace (U.S.)

- Eaton Aerospace (U.S.)

- GESIPA Aerospace (Germany)

- Henrob (U.K)

- Huck Aerospace (U.S.)

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Airbus (France) revealed a new range of lower-impact riveting equipment aimed at cutting waste and energy use in production. The move supports Airbus's sustainability targets and addresses tightening green-manufacturing regulations, while potentially improving its market standing with customers and stakeholders who prioritize environmental performance.

- July 2025: Lockheed Martin (U.S.) broadened its manufacturing toolkit by acquiring a smaller company focused on advanced riveting technologies. The deal is intended to expand Lockheed's technology base and help it respond faster to rising demand for next-generation aerospace manufacturing Types, strengthening its edge as the market shifts toward higher-tech capabilities.

- October 2023: GESIPA introduced the GBS 1000, a battery-powered, semi-automatic blind rivet setter built for lightweight to medium-duty tasks. It combines a brushless motor, a user-friendly ergonomic form factor, and a simple, intuitive interface for smoother day-to-day operation.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies across key regions of the industry. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026-2034 |

| Unit | Value (USD million) |

| Segmentation | By End Use, By Equipment, By Type, By Technology, and Region |

| By End Use |

|

| By Equipment |

|

| By Type |

|

| By Technology |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,631.0 Million in 2025 and is projected to reach USD 2,914.1 Million by 2034.

In 2025, the market value stood at USD 595.15 million.

The market is expected to exhibit a CAGR of 6.4% during the forecast period.

Based on end use, the OEM segment is expected to dominate the market.

Demand for lightweight materials and precision assembly driving market growth.

Airbus Helicopters (France), Avdel (U.K), Boeing Commercial Airplanes (U.S.), Cherry Aerospace (U.S.), and Eaton Aerospace (U.S.) are a few major players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us